Advertiser Disclosure Numerous or all of the items featured here are from our partners who compensate us. This might affect which products we compose about and where and how the item appears on a page. However, this does not influence our examinations. Our opinions are our own. After retirement, without routine income, you may in some cases have a hard time with finances.

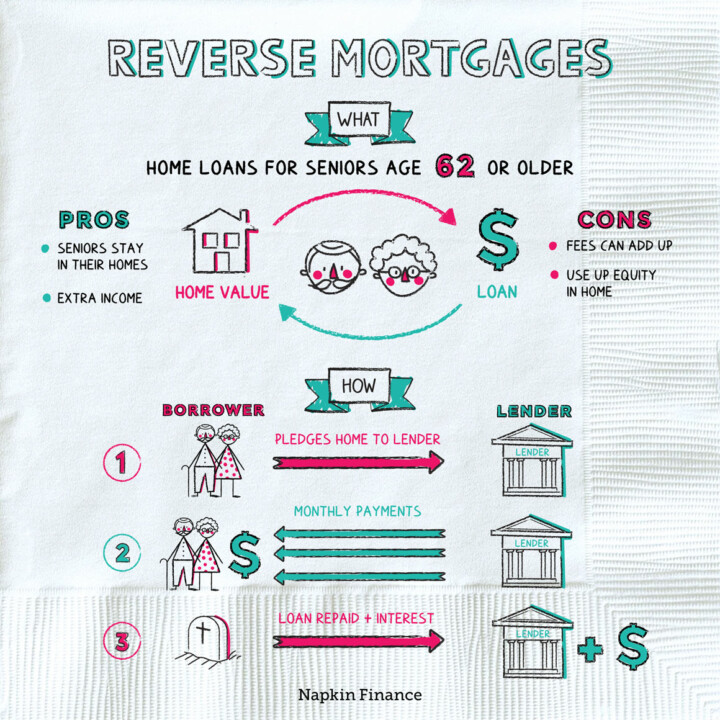

A reverse home loan is a house loan that enables property owners 62 and older to withdraw some of their home equity and transform it into cash. You don't need to pay taxes on the proceeds or make regular monthly mortgage payments. You can use reverse home loan profits nevertheless you like. They're often earmarked for expenses such as: Debt consolidation Living costs House improvements Assisting children with college Buying another home that may Have a peek at this website much better fulfill your requirements as you age A reverse home loan is the opposite of a standard mortgage; rather of paying a loan provider a regular monthly payment monthly, the lending institution pays you. You should participate in counseling, a "consumer information session" with a HUD-approved counselor, prior to your HECM loan can be moneyed. This rule is intended to guarantee that you comprehend the expense and effects of securing this kind of loan. Therapists work for independent companies. These courses are offered at a low expense and in some cases they're even complimentary.

For many borrowers, this indicates paying off your staying home mortgage debt with part of your reverse mortgage. This is most convenient to attain if you have at least 50% equity approximately in your home. You have a couple of alternatives, but the easiest is to take all the cash simultaneously in a swelling sum. what are today's interest rates on mortgages.

You can also pick to receive routine routine payments, such as when a month. These payments are described as "tenure payments" when they last for your entire life time, or "term payments" when you receive them for just a set amount of time, such as 10 years. It's possible to take out more equity than you and your loan provider anticipated if you select period payments and live a remarkably long life.

This permits you to draw funds only if and when you require them. The benefit of a line-of-credit method is that you just pay interest on the cash you've really obtained. You can likewise utilize a mix of payment alternatives. For instance, you may take a small lump sum upfront and keep a credit line for later on.

For example, the home will go on the marketplace after your death, and your estate will get cash when it sells. That money that should then be utilized to settle the loan. The full loan amount comes due, even if the loan balance is greater than the house's value, if your heirs decide they want to keep the home.

The 8-Second Trick For How To Swap Houses With Mortgages

Numerous reverse mortgages include a stipulation that does not allow the loan balance to surpass the value of the home's equity, although market changes Learn here may still result in less equity than when you got the loan. It's possible that your estate might supply enough other possessions to enable your heirs to settle the reverse home loan at your death by liquidating them, however they may otherwise not be able to receive a regular home mortgage to settle the debt and keep the household home.

You'll pay a lot of the exact same closing costs required for a conventional home purchase or re-finance, however these charges can be greater. Costs reduce the quantity of equity left in your house, which leaves less for your estate or for you if adam wessley you choose to offer the home and pay off the home mortgage.

Charges are frequently financed, or constructed into your loan. You do not compose a look for them at closing so you may not feel these costs, however you're still paying them regardless. You should have your house assessed, contributing to your expenses. The lending institution will wish to make certain that your home in good shape prior to composing the loan.

A reverse mortgage lets older house owners tap into their house's equity for a swelling sum payment, routine payments, or in the kind of a credit line. Reverse home mortgages do not have to be repaid until the property owner dies or moves out of the home. Remains in care facilities for less than a year are all right.

Interest accrues over the life of the loan, so the quantity required to settle the home loan will likely be substantially more than the initial loan earnings - what are the different types of mortgages.

A reverse mortgage is a method for homeowners ages 62 and older to utilize the equity in their house. With a reverse mortgage, a house owner who owns their home outright or a minimum of has significant equity to draw from can withdraw a portion of their equity without having to repay it up until they leave the home.

The 6-Minute Rule for Which Type Of Organization Does Not Provide Home Mortgages?

Here's how reverse home loans work, and what property owners considering one requirement to understand. A reverse mortgage is a type of loan that allows homeowners ages 62 and older, generally who have actually paid off their home mortgage, to obtain part of their home's equity as tax-free earnings. Unlike a regular mortgage in which the property owner makes payments to the loan provider, with a reverse mortgage, the lending institution pays the homeowner (why do mortgage companies sell mortgages).

Among the most popular types of reverse home mortgages is the Home Equity Conversion Home Mortgage (HECM), which is backed by the federal government. Regardless of the reverse home mortgage concept in practice, qualified homeowners might not be able to obtain the entire worth of their home even if the mortgage is settled.